Answers to the most important questions

About CG24 Group

General

What is CG24 Group?

CG24 Group is an online credit platform (peer-to-peer) which connects borrowers with investors quickly and efficiently. Investors and borrowers alike enjoy the benefits of lower and transparent costs compared to traditional banks and other credit providers. Borrowers benefit from flexible, fast and low-cost loans as well as a simple and straightforward loan review process. At CG24 Group, discretion and the protection of personal data is top priority. Investors have the opportunity to invest in various credit projects with different risk and return profiles (rating levels). We support the security of investors through strict and elaborate risk assessment. We implement distinctive hedging measures such as death benefits insurance and a high degree of diversification to facilitate return potential.

What are peer-to-peer loans?

Peer-to-peer loans (P2P) are loans between two parties; e.g., from private individual to private individual. Loans are granted directly via an internet platform without a financial institution acting as an intermediary. P2P loans restore the social component that has been lost due to centralised banking.

What doCG24 Group’s services cost?

CG24 Group receives a fee from investors and borrowers for quality control, platform use and support during the term of the loan. Depending on the term and the product, the fee for borrowers is a one-off 0.75 - 3.6% of the loan amount received and for real estate loans an additional 1% periodic service fee. Investors are charged a fee of 0.25 - 2.726% on the actual repayments (including amortisation and interest payments) made by the borrower to the investor, depending on the term, rating and product.

What fees does CG24 Group charge?

Why does Hypothekarbank Lenzburg recommend CG24 Group to its clients?

Hypothekarbank Lenzburg offers its clients the possibility to conclude personal loans directly via CG24 Group’s online platform. The cooperation is in the interest of the clients who benefit from the low interest rates and flexible solutions of CG24 Group. Marianne Wildi, CEO of Hypothekarbank Lenzburg says: "We can recommend the CG24 platform to our clients with a clear conscience - both for borrowers and lenders." (Press release cooperation with CG24 Group)

What payment options are available?

CG24 Group uses the new QR invoice standard for invoices for investment amounts and loan instalments/repayments. As a CG24 Group client, you can also conveniently pay your invoices via Debit Direct (Postfinance) or LSV (other banks). You can enter the desired payment method in your profile. If you have any problems, we will be happy to advise you on +41 44 244 30 24.

Does the change from CreditGate24 (Switzerland) Ltd. to CG24 Group Ltd. affect me?

No. This change has no effect on the clients or on the cooperation. Please note that you will be required to use the new address, CG24 Group AG, Letzigraben 89 in 8003 Zurich, for invoicing purposes.

Business Credit

General

What advantages does CG24 Group - Business Credit offer me?

CG24 Group Business Credit offers a quick and easy way to finance Swiss SME companies via a crowdfunding platform. You can choose a flexible financing amount as well as a flexible term. For repayment, we offer various options such as amortisation, bullet lending or a combination of these. CG24 Group also attaches great importance to clear and transparent pricing.

What products does CG24 Group offer for companies?

We are constantly working on improving our product range. We currently offer the following products to our SME clients:

Customer service

Who should I contact if I have any questions?

Your personal customer advisor will be happy to answer your questions and concerns. If you are new to us, please feel free to contact us by phone (+41 44 585 38 50), using our chat or by email (corporate@cg24.com). If you would like us to contact you, you can make a telephone appointment with an account manager here at any time. Click here to view contact form.

Data protection

Who has access to my data?

You can read about what data CG24 Group collects in our privacy policy.

Where is my data stored?

You can read where your data is stored in our privacy policy.

What data does the CG24 Group collect about me?

You can read which data the CG24 Group collects in our privacy policy.

Registration - Requirements

What are the minimum requirements for an SME loan?

Your business must be at least two years old and have at least two completed balance sheets and profit and loss accounts.

Unfortunately, we cannot serve companies that do not meet these minimum requirements. Furthermore, we can only accept companies that have an annual turnover of at least CHF 100,000.

What documents do I need to have ready to open an account?

As we need to carry out a successful credit check, we require a number of documents about your company, such as the annual financial statements for the last 2 years and detailed account statements for the last 3 months.

My company is still in the start-up phase. Can CG24 Group already help me?

Your company must be at least two years old and have at least two completed balance sheets and profit and loss accounts. Unfortunately, we cannot serve companies that do not meet these minimum requirements.

Registration

Why is my email address not accepted?

CG24 Group requires a professional email address as a basic requirement for companies. For example, addresses ending in @hotmail, @bluewin, @gmail etc. cannot be accepted. Feel free to contact us again after creating a new email address online with your company name.

What are the costs for registration?

Registration is free of charge.

What documents do I need to have ready to open an account?

We require a number of documents for a successful credit check. We cannot grant financing to companies that do not provide us with any documents.

The following documents must be provided by clients:

- Annual financial statements for the last 2 years.

- Bank statements for the last 3 months.

- Other documents that are relevant from the client's point of view (e.g., order confirmations, contracts, invoices).

Further information besides what is listed above may be required for credit assessment. Your account manager will contact you if necessary.

How long does it take to create an account?

It takes no more than five to ten minutes to create your profile on CG24. Your profile will then be checked before it can be verified.

How do I create an account with CG24 Group?

Click here to view registration

Identification

How does identification work on the platform?

CG24 Group identifies all users by video verification.

The verification process is carried out by IDNow GmbH. This process takes approximately five minutes. Please note that CG24 Group currently only accepts ID cards or passports from Switzerland, the European Union, Turkey, Norway and Iceland.

If a person not authorised to register on behalf of an SME registers, a corresponding power of attorney for this person must be submitted. CG24 Group can provide a template for the power of attorney if required.

Why do I need to identify myself to CG24 Group?

For legal and regulatory reasons, CG24 Group is required to carry out identification of the potential new client prior to entering into any client relationship.

Check

How is my creditworthiness determined?

Your credit rating and credit limit are calculated based on the financial information about your company. An individual review by our credit specialists then leads to the final decision on your credit limit and credit rating. The decisive factors are qualitative and financial information on creditworthiness and credit standing, external credit reports and other factors such as the possible deposit of collateral.

We apply the highest degree of discretion during this process to ensure that our assessment does not affect your business in any way. In doing so, we do not contact third parties (with whom you do business) or financial institutions.

Why was my account rejected?

Profiles that do not meet the following requirements will be rejected by CG24 Group:

- Lack of creditworthiness

- Company does not meet the requirements for using the platform (e.g., no entry in the Swiss Commercial Register, annual turnover of less than CHF 100,000, was founded less than two years ago).

- Other reasons not explicitly listed here (e.g., failure to submit the required documents, falsification of documents, etc.)

However, it is possible to have your profile re-evaluated after three months. If there is a significant change with regard to the reason for rejection, it is possible to have your profile reviewed after 3 months. Please send us an email with your request to the following address: corporate@cg24.com.

How long does the review of my account take?

In most cases, the review is completed within 48 to 72 hours. For complex cases or missing documents, it can take up to a week.

What factors determine my creditworthiness?

The following criteria determine your creditworthiness:

- Company credit reports from external credit bureaus.

- Annual reports for the last 2 financial years

- Bank statements for the last 3 months

- Repayment history within the last 12 months

- Other qualitative factors

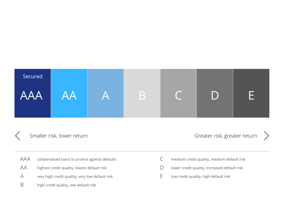

Your credit rating ranges from A (lowest risk of default) to E. It determines whether we can grant you access to the platform and what financing conditions you will ultimately receive.

E-signature

CG24 uses Swisscom's QES technology for signing contracts. Swisscom is the official provider of "Qualified Electronic Signature" (QES) technology in Switzerland.

What is a qualified electronic signature (QES)?

The qualified electronic signature (QES) is an electronic signature that is equivalent to a handwritten signature. It makes it possible to sign contracts with formal requirements online.

How can I tell that a document is signed with QES?

A qualified electronic signature can be seen on the cover sheet of the contract. The validity of the signature can be checked directly in Adobe Acrobat Reader or using the government’s online service (www.e-service.admin.ch/validator).

What advantage does QES offer me?

Thanks to QES, contracts can be signed digitally, which leads to faster processing.

How does QES work?

With QES, the signature is created in combination with an identification. Thanks to this identification, the signature can be assigned to exactly one person. Once the identification has been confirmed, the signature is created from a combination of password and SMS.

Financing

How long does it take until I have the funds on my account?

All new approved funding requests are offered to our investors on the platform and are usually refinanced within 2-5 days. The pay-out time is determined by the time of complete funding by the investors. We transfer the money to your company during Swiss bank working days no later than 24 hours after receiving the investment funds. As a rule, you can expect payments to be credited to your account within 24-48 hours once we have received the money from the investors.

What are the costs and fees?

The platform is structured transparently. In addition to the monthly interest, you will be charged a one-time upfront fee and an annual service fee. These fees depend on the loan volume, the term and your rating. A minimum fee in the amount of CHF 750 is mandatory.

What credit periods are possible?

The credit term is between 1 and 36 months. A longer term may be possible in individual cases.

What is the minimum credit amount?

The minimum credit amount is between CHF 10,000 and CHF 15,000, depending on the product.

In which currencies can the transactions be processed?

All transactions are processed exclusively in Swiss francs (CHF).

Credit limit

How long is the credit limit valid?

The credit limit is subject to annual review. The credit limit is then generally valid again for 12 months, although interim adjustments can be made under certain circumstances.

What does the credit limit mean for me?

The credit limit corresponds to the maximum possible financing potential of a company. The limit can also be divided between different types of financing (minimum amount of financing is CHF 10,000).

How much financing can I receive from CG24?

CG24 Group provides you with a credit limit after successful registration and credit assessment. Within this credit limit, you can take out one or more business loans with different amounts and terms (the minimum amount of a business loan is CHF 10,000).

The credit limit depends on factors such as qualitative and financial information about your business and external credit reports.

The final credit limit can only be calculated after CG24 Group has thoroughly reviewed your company.

Signing the agreement

When is the agreement signed?

Loan agreements are subject to the condition precedent that the loan amount has been financed by investors. Suspensive agreements are only validly concluded when the conditions precedent have been fulfilled.

Which agreements must be signed?

All agreements must be signed by hand or with a qualified electronic signature (QES).

Repayment

What costs are incurred in the event of late payment?

Default interest will be charged two days after a missed payment date. Notice fees are charged after 14 days and 30 days following a missed payment date.

What if I cannot repay?

Please contact your customer advisor at an early stage if you are experiencing payment difficulties. We will be happy to help you work out a solution tailored to your individual situation.

When do I have to repay the outstanding financing?

The repayment date is agreed in each case when the agreement is concluded and is entered into the loan agreement. The repayment date is based on the disbursement date of the loan from CG24 to you.

Invest

Investors

Who can invest money with CG24 Group?

In principle, anyone can invest money with CG24 Group (certain domiciles such as the USA are excluded for legal reasons), although our primary demographic includes investors residing in Switzerland. You must be of legal age and have an account with a Swiss bank. CG24 Group is subject to the Swiss Money Laundering Act and is obliged to check the plausibility of all payment flows and, where necessary, to clarify the origin of the funds.

What is a Credit Project Share ("CPS")?

The CPS stands for an investor's share in a specific credit project. It is defined by its amount, term, interest rate and rating.

What is the minimum investment amount per credit project?

The minimum investment amount per credit project is CHF 500.

How do I invest with CG24 Group?

The minimum investment amount per credit project is CHF 500. Investing money with CG24 Group is simple and quick. You register via the Swisscom online identification procedure. Once we have successfully checked your details, we will activate your account. You are now set up to generate lucrative returns:

-

under the menu item "Invest money" -->"New investment opportunities" you will find an overview of all currently available loan projects, their rating level, nominal interest rate, term and yield, as well as anonymous information about the borrower and intended use.

-

select your loan project(s) based on your preferences.

-

determine the amount you want to invest.

-

click on the button "Confirm investment bindingly". Now your investment becomes binding.

-

as soon as your investment has been confirmed, you will receive the invoice and the investor agreement; these are also available as a download in the investor cockpit. The deposit can also be made via LSV+/DD.

Does it matter from which account my deposits come?

Yes, the deposit must be made from the registered Swiss account.

How do I receive my earnings?

As an investor, your earnings (interest plus amortisation) are credited directly to your account via CG24 Group after the transfer by the borrower and transferred to your external reference account (bank or postal account).

What fees do I pay as an investor?

What advantages does the CG24 Group offer me as an investor?

Investors can invest individually in different credit projects with very attractive risk and return profiles (rating levels). In doing so, you support people and their projects. CG24 Group brings investors together with borrowers and, thanks to its online structure, saves high costs of traditional loan providers. Both investors and borrowers benefit from these cost savings. The risk for investors is reduced as much as possible through the following measures:

- Every loan is subject to a strict and elaborate risk assessment.

- Depending on the loan, the borrower takes out a death benefits insurance policy that covers a theoretical residual debt loss of CHF100,000. (The borrower's specific circumstances must be taken into account and may lead to restrictions with regard to the insurance benefit).

- The borrower can also take out disability and unemployment insurance (PPI - Payment Protection Insurance or credit default insurance).

- Minimising the impact of a loan default for individual investors by distributing loan defaults among all investors within the same rating level and loan type (loan default pooling).

- Strict monitoring of all payment flows and consistent receivables management.

Since, despite these measures, not all risks can be completely ruled out, we recommend that you spread your investment over different projects in the same rating level or in other rating levels across different types of credit (SME instalment loan, personal loan, SME short-term loan and real estate loan) in order to minimise the risk.

What does "additional return opportunity" mean?

Additional return opportunity corresponds to the expected probability of default of the loan and is included in the monthly payment.

What is the gross yield?

The gross yield is the yield before deducting the investor service fee and the statistically expected defaults.

What does "maximum net yield" mean?

The maximum net return is the return after deduction of the service fee, without taking into account any defaults.

What does "expected net return" mean?

This means the return after deduction of the service fee, including consideration of any expected defaults.

Will I receive a tax statement from CG24 Group?

Yes. CG24 Group produces a detailed tax statement annually. We recommend that you only include the total amounts in your tax return and attach the printed tax statement. CG24 Group does not charge any additional costs for the preparation of the tax statement.

What does the amount of the joint and several liability listed in the tax statement mean?

The amount of the joint and several liability listed is the total of the joint and several liability incurred in the tax year, irrespective of the actual debit. The decisive factor is therefore the time when the joint and several liability arises (= time when the joint and several liability is notified) and not when the joint and several liability amount is offset against an instalment repayment.

What does the amount of recoveries listed in the tax statement mean?

Recoveries of defaulted loans (e.g., if a borrower has funds again and CG24 Group is in possession of a loss certificate, this can be claimed) are paid out to the joint and several liability holders concerned. The amount shows the recoveries paid out in the tax year.

Investor Cockpit

What can I find in the Investor Suite under "Portfolio" in the statistics section?

Within the "Statistics" section, the portfolio shows the current status of your investments with CG24 Group. This figure includes the outstanding capital amount, i.e., the total of your investments minus the amortisation payments already made. Also included and referred to as "cash in transit" are investor contributions that have already been paid in but not yet disbursed to the borrower.

What is the composition of net income?

Net income includes all interest and other income received to date, less any solidarity contributions charged. The investor service fee is not reflected.

How is return determined?

The return shows the effective annual return for your portfolio. It takes into account the amount of capital invested, capital amortisation, interest income, compensation and fees, accrued interest, debits and credits from solidarity contributions and premiums from secondary market transactions. The calculation is based on an internal rate of return (IRR) method that takes into account daily historical as well as expected cash flows.

What does the status of my investment mean in detail?

- Investment: The investor has committed a contribution but the loan is not yet fully funded. The loan is on the CG24 Group platform until it is fully funded.

- Rejected: The borrower has withdrawn from the agreement within the statutory period.

- Money demand: The loan is fully funded, the investors have received the deposit invoice.

- Loan disbursement: All investors have transferred their shares, disbursement is in progress.

- On time: The borrower has paid all instalments due.

- 1 - 30 days overdue: An instalment is up to 30 days overdue. First measures have been taken.

- 31 - 60 days overdue: An instalment is up to 60 days overdue. Further action has been taken.

- 61 - 90 days overdue: A rate is up to 90 days overdue. Measures have been intensified.

- More than 90 days overdue: An instalment is more than 90 days overdue. Further measures, possibly legal action, have been initiated.

- Early repayment pending: The borrower has exercised his right to early repayment. Repayment is expected within 30 days.

- Repaid early: The borrower has repaid the loan early.

- Terminated: The loan has been repaid in full.

- Sold: The loan has been sold on the secondary market.

- Default with chance of recovery: The loan has been declared uncollectible. A subsequent realisation of the loss certificate is pending.

- Default with loss: The loan has been declared irrecoverable. The amount is considered to be definitely in default.

Secondary Market

What is the CG24 Group Secondary Market?

The Secondary Market allows CG24 Group's registered investors to sell their investments (CPS: Credit Project Share / loan shares) before the end of the term and thus recover their loan amount, which has not yet been fully repaid at that time, ahead of time. The secondary market also allows investors to buy a CPS (Credit Project Share) in existing credit projects with a shorter remaining maturity.

What can be offered or bought on the secondary market?

On the CG24 Group Secondary Market, investors can buy and/or sell individual already financed CPS (Credit Project Shares) before they are fully repaid. A CPS must have a remaining term of at least three months at the time of the decision to sell and the corresponding listing on the secondary market. In general, CPS can only be offered for sale if the corresponding loan has no arrears.

Who is eligible to buy or sell CPS (Credit Project Shares) on the secondary market?

The CG24 Group Secondary Market is open to all registered investors of CG24 Group.

Who determines the price of a CPS (Credit Project Shares) on the secondary market?

By default, the purchase price is based on the amount outstanding to the original investor at the time of sale. However, the seller is free to demand a slightly higher or lower purchase price. All relevant information on the CPS will be disclosed to the potential new investor/buyer. In the interest of investor protection, CG24 Group reserves the right to delete offers with unrealistically high sales prices from the secondary market. For this purpose, the buyer’s return of the CPS offered in the secondary market is compared with a new loan with the same or similar characteristics.

How is a purchase or sale on the secondary market handled?

Investors who wish to sell one or more of their credit shares (CPS) can enter the order to do so in their suite. As soon as a buyer for the offered CPS is found and transfers the purchase price, the CPS is transferred and the seller receives his money. If the buyer does not transfer the purchase price on time, the sale "falls through" and the CPS remains with the original investor. It can be put up for sale again on the secondary market at any time.

What happens to borrower amortisation and interest payments received during the sale process?

Investors who have recorded a CPS for sale will continue to receive all of the borrower's amortisation and interest payments until such time as a buyer purchases the CPS. Payments received from this point onwards will be paid to the buyer once the sale has been successfully completed. The purchase price is adjusted accordingly so that the respective invoiced purchase price correctly reflects the cash flows. In the event of a bounced sale, all cash flows go to the seller.

What happens if a loan defaults while a CPS (loan shares) is for sale?

The CPS can no longer be sold at that point and the offer is automatically removed from the secondary market by CG24 Group.

Are there any restrictions on selling a CPS (loan share) on the secondary market?

A CPS cannot be sold if at the time of the sale an instalment payment had to be reminded to the borrower.

Recovery

What do we mean by recovery?

By recovery we mean all measures that serve to reduce payment arrears or to repay the credit debt. The recovery process begins when reminders have not led to the expected payment.

What happens if a debtor does not pay his instalment?

On the third day after the due date, the debtor is sent a payment reminder. This is followed, if necessary, by a first and a second reminder.

Are investors informed about payment irregularities?

We inform investors about payment delays and measures taken. The first notification is made when an instalment collection procedure has been initiated. In addition, investors can find out about payment arrears in the Investor Suite under the menu item "Investments".

What happens if the client does not respond to instalment reminders or does not pay the instalment?

We initiate debt collection for the monthly instalment due.

Can CG24 Group cancel the loan if the debtor does not pay his instalments?

If a loan is subject to the Consumer Credit Act (loans to private individuals up to CHF 80,000), CG24 Group may only terminate the loan if the outstanding instalments amount to at least 10% of the loan amount.

For all other loans, CG24 Group has the right to terminate the loan in the event of late payment. We make this decision in the best interest of our investors.

Are reminders associated with costs for the debtor?

Yes, for reminders we charge a contribution margin for our expenses. The reminder fees are listed in our fee regulations.

When is a loan designated as uncollectible?

Uncollectability is determined by CG24 Group when all measures taken to repay the debt have been unsuccessful. This is usually the case after receipt of a loss certificate.

Does an investor lose his stake if a loan in which he has invested is determined to be uncollectible?

No. In this case, joint and several liability comes into effect. All investors who have invested in the same type of loan and the same rating level jointly and severally assume a share of the default incurred.

How is the amount of joint and several liability calculated?

The defaulted loan amount (including the costs of legal action) is set in relation to the total loan amount of the entire loan type and rating level. The resulting percentage is used to calculate the joint and several liability amount.

Example:

|

Defaulted credit amount incl. costs |

CHF 7,500 |

|

Total of category/rating level |

CHF 1'200'000 |

|

Default in % |

0.63% |

Each investor in the same credit category/rating level is now charged 0.63% of the capital balance of his investment(s).

How are the solidarity contributions charged?

The calculated solidarity contributions are deducted from the next payment for an investment in the corresponding credit category and rating level.

What happens to loss certificates?

Claims from loss certificates can be asserted for 20 years. Depending on the assessment, CG24 will try to sell loss certificates or manage them.

What happens to any proceeds from loss certificates?

These will be refunded to the investors in proportion to the solidarity contributions made at the time.

Who is liable in the event of a loan default in the case of pending secondary market sales?

The seller is liable for a default on a loan of the same credit type and rating category of the investment being sold until the investment is fully transferred (receipt of the purchase price for the receivable by CG24 Group).

Rating and credit assessment system

What is the rating system?

What is risk optimisation through solidarity agreement?

In order to further minimise the default risk, CG24 Group has introduced risk pooling through a so-called solidarity agreement. In this way, the investor achieves the highest possible risk diversification without having to invest in dozens of credit projects.

Despite all hedging measures, a loan default can occur and loan recovery can be unsuccessful. If a loan defaults, the loss of the loan amount is distributed proportionally among all investors in the same rating level. In this way, the individual is only minimally affected in the event of a default and the expected return on the individual investment is ensured in the best possible way. Nevertheless, to minimise risk, CG24 Group recommends that investors invest in several projects, as even with the solidarity clause it can take several weeks for the affected investor to receive the solidarity contributions in the event of default.

What is the death benefits insurance?

Depending on the loan, the borrower takes out a death benefits insurance policy that covers a theoretical residual debt loss of CHF 100,000. The borrower's specific circumstances must be taken into account and may result in restrictions on the insurance benefit.

What is PPI?

The borrower can take out additional disability and unemployment insurance (PPI - Payment Protection Insurance or credit default insurance). This insurance serves the following purpose:

- The client receives the security of being exempt from paying his monthly loan instalments for a period of 12 months in the event of a loss of employment or incapacity for work through no fault of his own.

- At the same time, CG24 Group or the investor of the loan receives the full instalment for a period of up to 12 months in the event of a benefit claim.

What does credit assessment mean?

In addition to internal creditworthiness data and data provided by external providers, debt collection information and specific clarifications of the borrower are used.

Real Estate

General

What is subordinated financing?

Subordinated real estate financing - also called mezzanine financing - describes a loan secured by a real estate lien in addition to the existing 1st or 2nd rank mortgage, which is usually granted by a bank.

For whom is real estate financing from CG24 suitable?

Our real estate financing is aimed at professional (institutional or private) real estate investors with an existing portfolio of investment properties.

What type of property can I subordinate with CG24?

Subordinated loans are granted on rented properties (investment properties) in the residential sector with a maximum commercial share of 30%. These are usually apartment buildings, but rental flats are also suitable.

How is real estate financing secured?

Real estate financing is secured by establishing a subordinate mortgage over the entire loan amount, for example a registered or paper bearer mortgage.

How high can the property be additionally mortgaged?

An existing property can be additionally mortgaged up to a maximum of 80% of the market value, whereby own funds are released, for example, in order to be able to acquire further properties or to repair existing ones.

What is the advantage of real estate financing through CG24?

- Mortgaging up to 80% LTV, no amortisation obligation for mortgages above 65% LTV, no lower of cost or market principle, simple application process, individual advice, fast appraisal and processing

- Flexible terms of up to three years

- Additional equity in the shortest possible time and liquidity for your growth

How can I apply for real estate financing?

You are welcome to send us your request directly by email to our Real Estate Team (real-estate@cg24.com) or apply for the desired financing on our platform under the following link: Link

Can CG24 also finance real estate abroad?

No, our real estate financing is intended for borrowers domiciled in Switzerland and real estate located in Switzerland.

What is the minimum amount for a real estate financing?

The minimum amount for a real estate financing is CHF 100,000.

What documents are required for the assessment of a real estate financing?

- Documents relating to the property:

- Tenant schedule

- Extract from the land register

- Property statement

- Existing mortgage agreements

- Building insurance certificate

- Pictures and floor plans

- documents relating to the borrower:

- ID copy

- Tax return

- Annual financial statement

- Depending on the complexity and scope of the application, further documents may be requested.

Does the loan have to be repaid during the term?

No, the repayment is final, which means that the entire loan must be repaid at the end of the term. Interest and fees are invoiced quarterly or semi-annually. If you would like to repay the loan during the term, this can be discussed individually.

Can I also repay the loan early?

Yes, but the interest for the originally agreed term including the early repayment penalty must be paid.

How high is the interest rate?

Depending on the rating and term, the nominal interest rate is between 2.5% and 6.5% per annum.

What are the fees?

The credit check is free of charge.

When the loan is disbursed, the service fee (depending on the loan amount) is deducted directly. In addition, an administration fee is charged quarterly.

Click here to view the fee table

What are the possible terms for real estate financing?

A term of between 6 and 36 months can be selected for real estate financing.

How long does the process take from appraisal to disbursement?

Provided that all the necessary documents have been submitted, approval can be obtained within 48 hours. The duration of the subsequent financing of the loan depends on our investors, the loan amount and its rating. Usually, the financing period is between one and a maximum of three to four weeks.

Can I also apply for real estate financing for my clients as an agent?

Yes, of course. Contact us by email (real-estate@cg24.com) or phone and we will guide you through the process.

Can I also apply for first-ranking financing with CG24?

You are welcome to contact us regarding first ranking financing. You can enter your request under the following link: Link

We will forward your request to our associate who will obtain the best offer for your desired senior mortgage. If you have any questions, please do not hesitate to contact us on 044 244 30 22.

Do you have any further questions?

If you have any further questions, please do not hesitate to contact our real estate specialists at wenden:real-estate@cg24.com.

Will my personal data and documents be treated confidentially?

To the terms of use

To the data protection regulations

Private Credit

General

Who is CG24?

CG24 Group AG ("CG24") is an online credit platform (peer-to-peer). We connect credit seekers with investors - quickly and easily. Investors and borrowers alike enjoy the benefits of lower and transparent costs compared to traditional banks and other credit providers. Borrowers benefit from flexible, fast and low-cost loans as well as a simple and straightforward loan review process. Discretion and the protection of personal data are top priorities at CG24.

Who can obtain a loan from CG24?

Basically, anyone can apply for a loan, provided that at least the following requirements are met:

- You are between 18 and 65 years old.

- You have held a B residence permit for at least one year or longer.

- You have a minimum income of CHF 3,500 from an employment relationship that has not been terminated.

- Successful credit, identity and money laundering checks.

How do I apply for a loan?

At CG24 you can apply for a loan quickly and easily, directly via this link:

- Fill out the credit application within a few minutes.

- Upload the required documents. You will be shown directly which documents are necessary for a complete credit check based on your credit application.

- Receive a non-binding credit proposal tailored to you from our credit experts within 24 hours.

If you have any technical difficulties, we will be happy to help you by phone on 044 244 30 24.

What does a loan cost?

The account opening and the credit check are free of charge and you can obtain a non-binding and individual offer at any time.

The effective annual interest rate (includes the nominal interest rate, the fee for the death benefits insurance and the service fee) is between 6.9% and 10.9%.

The individual costs for a loan will be shown to you transparently in a personal offer. The loan is repaid over a contractually agreed term with fixed monthly instalments. The conditions are set out transparently in the credit agreement.

How quickly will the loan amount be paid out?

You will receive feedback on your loan application within 24 hours. If your loan falls under the Consumer Credit Act (loan amount between CHF 500 and CHF 80,000 and no exclusion reasons according to the Consumer Credit Act), payment can only be made 14 days following the signing of the contract. Loans with a credit amount above CHF 80,000 can be disbursed within a few working days after receipt of the credit agreement signed by you. The prerequisite for loan disbursement is that all requirements for the loan are fully met and your project has been fully financed by our investors, which usually happens quickly.

What advantages does CG24 offer borrowers?

- Favourable financing: Effective interest rate from 6.9%.

- Fastest credit check: You will receive a full credit offer within 24 hours of your credit application.

- Understandable and transparent: Our aim is to make our products as understandable and transparent as possible.

- Sensible and suitable financing for your needs: We also examine special and complicated situations without reservation.

- Simple communication: We are there for you. Simply contact us.

Can a loan be repaid early?

Yes, you can repay your personal loan early. For legal reasons, we distinguish between personal loans that are subject to the Consumer Credit Act (KKG) and those that are not.

Early repayment of loans that are subject to the KKG:

In the case of consumer loans, borrowers can fulfil their obligations under the loan agreement early. In this case, the borrower is entitled to a waiver of the interest accrued on the unused credit period. Early repayment must be announced to us in writing 10 working days before the date of repayment.

Early repayment of loans which are not subject to the KKG:

Loans with a loan amount of more than CHF 80,000 (or any other KKG exclusion) may be repaid early by borrowers, but no earlier than 12 months after the loan disbursement. The intended early repayment must be announced to us in writing 10 working days before the date of repayment. An early repayment fee is owed in accordance with the loan agreement.

What does rescheduling or loan redemption mean?

If someone has taken out one or more loans, they can refinance the existing debt. If someone is paying high interest rates today, they can make significant savings by switching to a cheaper provider. Furthermore, debts can be bundled, which can lead to a reduction in monthly costs. The previous debts (loans, leasing obligations, credit card debts) are then paid off by a SINGLE new lender.

How does CG24 deal with fraud attempts?

In the event of any attempted fraud, CG24 will file a criminal complaint without exception. Our credit specialists are specially trained in fraud detection and are in contact with numerous institutions in order to quickly validate a suspicion and report it to the police.

What exactly is credit protection and how does it work?

Credit protection is a voluntary insurance against incapacity for work and unemployment that you can sign up for with us.

In case of incapacity to work (due to illness or accident) or involuntary unemployment, you can contact our insurance partner, provide the relevant proof and your monthly installment will be covered by the insurance during the entire period of unemployment, but for a maximum of 12 months per benefit case.

The insurance coverage ends with the ordinary or premature termination of the loan agreement, but at the latest with the repayment of the entire loan amount.